Suppose you believe that the market is going to go down, what would you do? The normal answer is sell what you have and get out. However, what if you have nothing to sell? Until a couple of years ago, the answer would have been "Stay on the sidelines" for simple investors. The sophisticated investors always had plenty of avenues - shorting the stock, buying puts, selling naked calls, etc.

However, the gap was narrowed with the arrival of Inverse ETFs that allow even novice investors to short the market in a less risky way (you cannot lose more than what you put in the ETF, while in shorts your loss is theoretically unlimited and this can be psychologically unsettling for some). However, the power and pitfalls of these instruments are poorly understood by many, particularly by the long term investors. The power is obvious - you can go 1/X or 2/X of the market pretty easily, leaving all the pesky details of achieving them to the ETF managers. Here are the pitfalls.

1. Inverse and Leveraged ETFs lose money over the long term

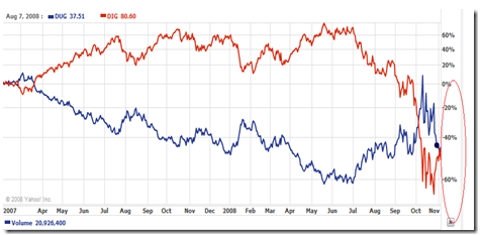

Here is the chart from Yahoo Finance of DUG (Double inverse of petroleum companies) and DIG (Goes 2X in the direction of petroleum companies). Basically they are the yin and yang of Oil industry. Regardless of what happens in the market surely one of them must win, right? But, look deeply at the cart - both of these funds lost 45% in the last 20 months.

So, even if you had predicted the correct direction, you would have lost half your money in just 1.5 years.

click to enlarge

2. Inverse ETFs can track the underlying for only one time period

Mathematically, leveraged and inverse ETFs can track their underlying index exactly for one time period only. If they track their index accurately for hourly, then it can't track for daily, weekly, monthly and so on. This is due to the way compounding works. Let us say your underlying went 1% down everyday for 1 month. The underlying will go down 26% [(1-0.01)^30], while your inverse would have gone up 35% [(1+0.01)^30]. Most inverse funds plan to track daily, so for other time periods you will see an error.

3. Tracking error increases with time

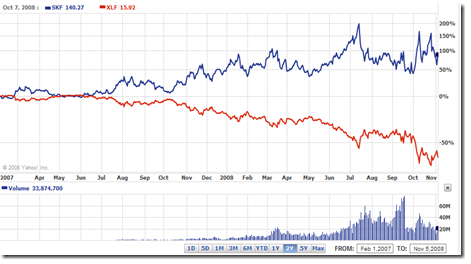

Here is the comparison chart between XLF (Financial Sector Index) and its double Inverse SKF. SKF is supposed to go 2X in the opposite direction of XLF, and though it was good in maintaining the direction, it was not very good in exact tracking. XLF fell 62% in the period from February 2007, while SKF has gone up only 90%, instead of 124% as would have been expected.

4. Degenerative decay and relationship to volatility

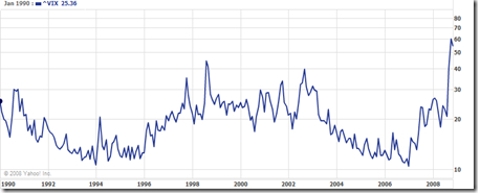

Leveraged ETFs' efficiency goes down with volatility. The problem is even more so with inverse ETFs. Let us say the Dow went from 10K to 8K and back to 10K. An inverse ETF tracking accurately will go up from 100 to 120 (20% gain to equal 20% loss in Dow) and then from 120 to 90 (25% loss because Dow gained 25%). So, from period t1 to t2, the Dow stayed the same, while its inverse ETF fell by 10% from 100 to 90. Repeat the same process x number of times, and you will find the inverse ETFs totally wiped out of the value, while underlying has not moved much. If the Dow goes up to 10000 from 9900 and back to 10000, the inverse would be reasonably accurate. However, we are at a historically high volatility - the highest in the last 20 years. Here is the movement of volatility Index [VIX] over the last 18 years.

5. Constant Leverage Trap

Constant Leverage Trap is a well know problem in financial modeling and affects the performance of inverse ETFs. Here is a simple scenario explained by Tyates in a financial forum:

Proshares has $1m of investor money and borrows $1m of additional money to invest $2m in the S&P 500 index. After six months, the index appreciates 10%, and then the fund has $2.2m in assets and $1.2m of equity. (Let's ignore interest on debt for now).

The problem is that the fund now has a lower debt to equity ratio than advertised. It is supposed to be a 2x fund, but now only has $1m of debt paired with its $1.2m of equity, making it a 1.67x fund. In order to get back to its target leverage it has to borrow $200,000 and invest in the index. Now the fund has $2.4m in assets and $1.2m in debt. Six more months go by, and the index falls 10%. The fund now has $2.16m in assets and $1.2m in debt, leaving the investors with $960k in equity. This 4% loss surprises investors who thought that the index was down 1% for the year (+10% and -10% = -1%).

But what happens next is even worse. Because the leverage ratio is out of balance again - total assets are 2.25x the equity, not 2x - the fund has to sell its shares in order to reduce its leverage back down to 2x. It sells $240k worth of shares, and applies all of this cash to reducing the debt to $960k. The fund is now smaller than when it started. Yes, you read that correctly, to maintain constant leverage, this index fund is constantly buying and selling, incurring short-term gains, and doing the worst possible market timing - buying more on margin when prices are high and selling when they're lower.

6. Regulatory Actions:

When the SEC comes up with a short ban as it did in September, it can substantially screw up the market. For a couple of weeks SKF was affected due to its inability to find appropriate counterparties for its trade. Typically, governments tend to go more after bears than bulls in a mistaken fear that bears are causing the problems instead of being the messenger of problem information. Thus regulatory actions can be more unfavorable to bearish strategies than bullish strategies.

http://biz.yahoo.com/ms/080919/253823.html

7. Counterparty risk

Inverse ETFs achieve their strategies through swaps and futures contracts with various counterparties. There are troubles when the counterparties don't honor their contract. When these parties fail, then the ETF could lose money.

Here is some good information on this, written by Paul Amery.

8. Other factors to consider

- Can you stomach the volatility? Double Inverse and Leverage ETFs tend to move enormously by definition, particularly in troubled times like these - you could see your portfolio going up or down 50 or 75% - even if it too heavily weighted in such ETFs. Will you have trouble sleeping well in such roller coaster activity? If so, you should not play.

- High Management Expense - given that these ETFs are not plain vanilla - buy a bunch of stock types, management expenses of maintaining leverage is pretty high. Sometimes the expense ratios can be up to 5X more than popular index ETFs.

Summary:

Inverse and leveraged ETFs are great tools that democratized bear strategies. However it should not be used for anything other than short term trading purposes. And when you use it, understand its risks and don't be surprised when you find the results are not as promised.

狗仔卡

狗仔卡 发表于 2009-1-13 05:30 PM

发表于 2009-1-13 05:30 PM

提升卡

提升卡 置顶卡

置顶卡 沉默卡

沉默卡 喧嚣卡

喧嚣卡 变色卡

变色卡 发表于 2009-8-5 05:02 AM

发表于 2009-8-5 05:02 AM