|

|

JPMorgan Chase (JPM) reported its quarterly earnings today. The headline was $2.1 billion in net income, beating analysts’ estimates. Behind the headlines, it was similar to the story that Goldman (GS) told earlier this week: a huge jump in fixed-income trading, status quo everywhere else, and continuing writedowns. For example, if you look at the breakdown of revenue by type of activity (not line of business) on page 4 of the supplement, you’ll see that revenue was flat or down in every category except one: principal transactions, where it jumped from a loss of $7.9 billion to a gain of $2.0 billion. That $9.9 billion improvement more than explains the entire increase in pretax profit from negative $1.3 billion to positive $3.1 billion.

As with Goldman, it was clearly a good quarter for JPMorgan; making money beats losing money any day. But the question to ask is whether it is sustainable, either for JPMorgan or for the banking industry as a whole. To answer that question, here are some pictures.

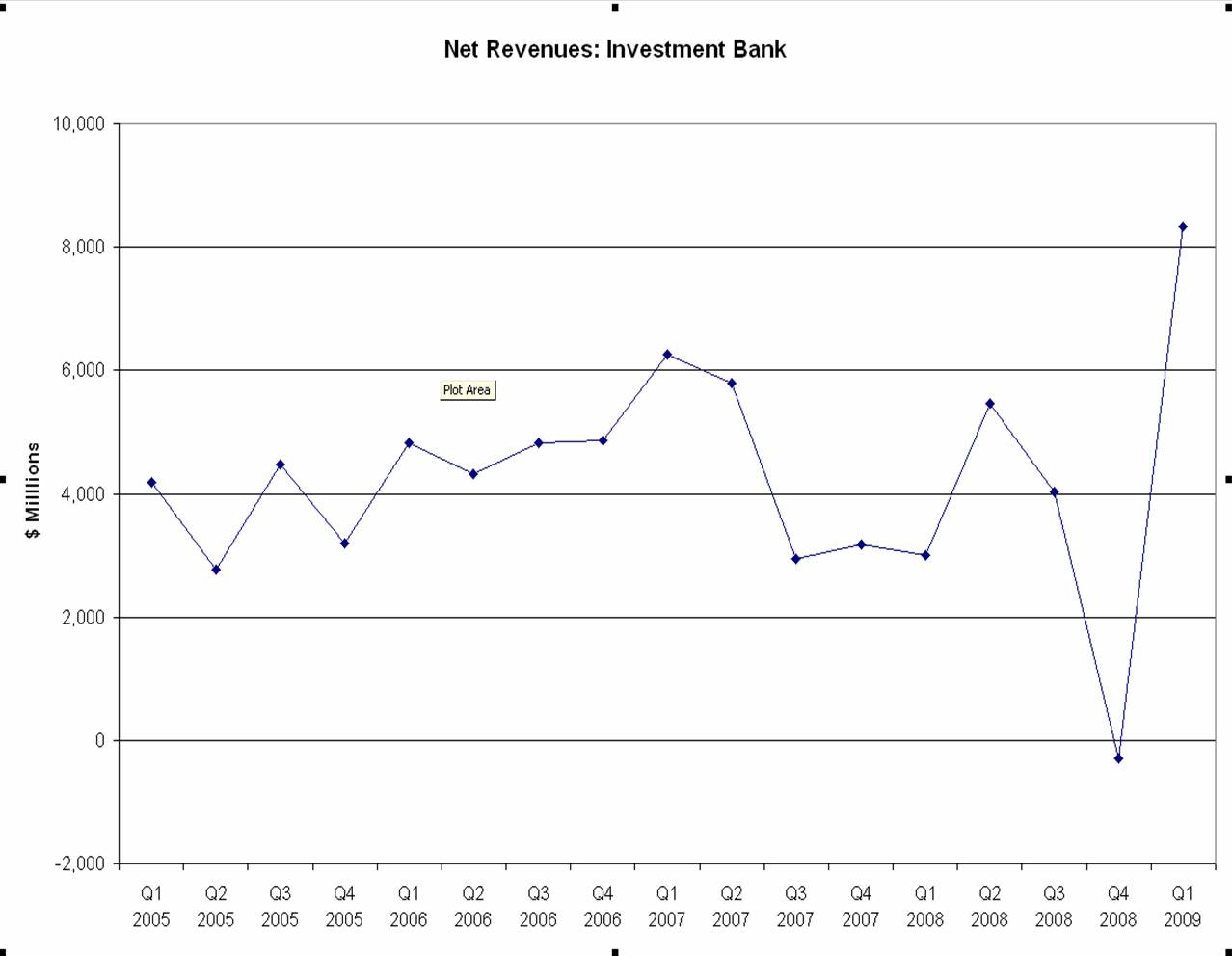

First, if you look at the net revenues on a line-of-business basis (page 8), you see that virtually all the improvement came from investment banking, which improved from negative $0.3 billion to positive $8.3 billion. Here’s that $8.3 billion in historical perspective. (All the charts below are on the same scale.)

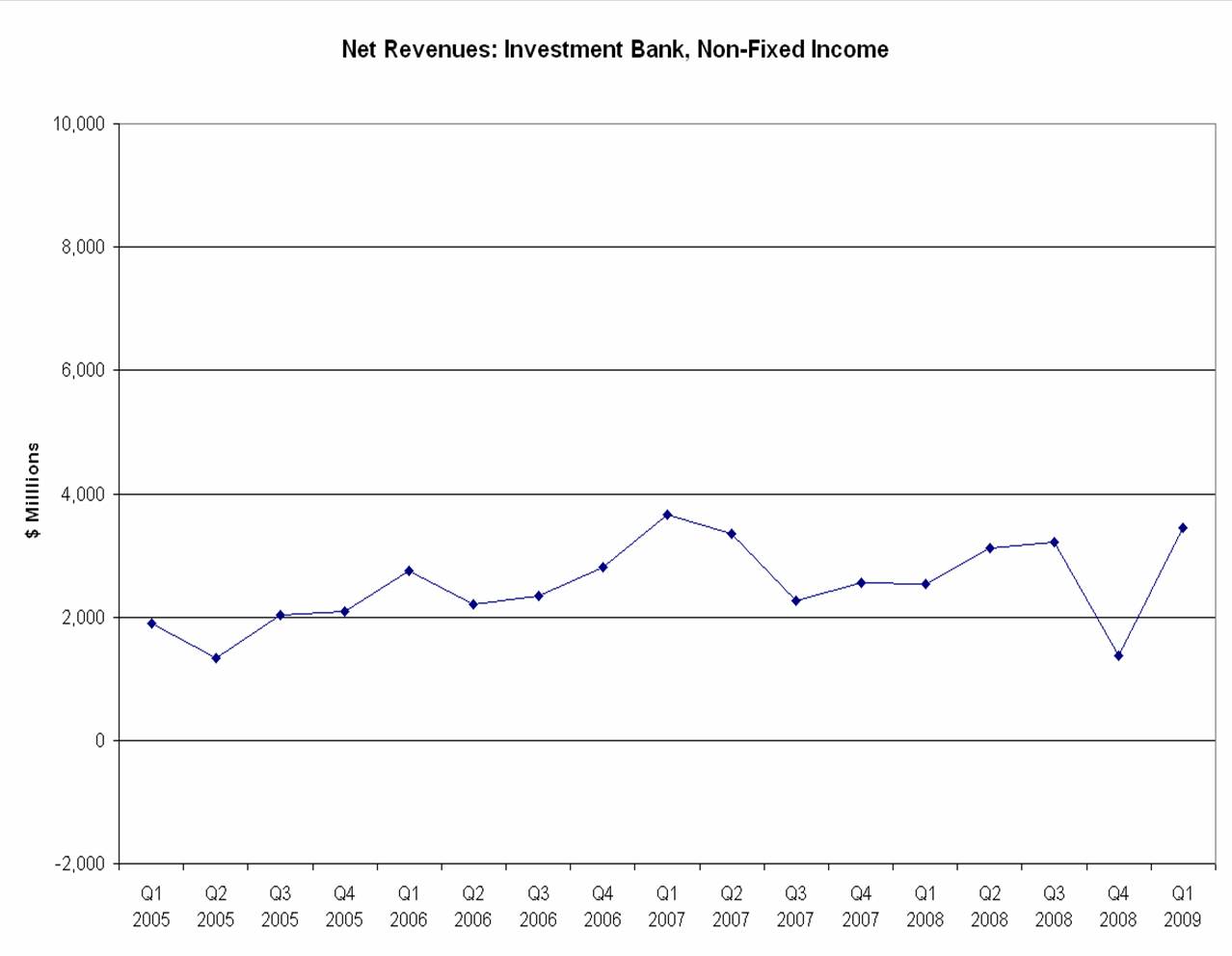

Now what was behind that super quarter? Here is the historical performance of all the investment banking business except fixed income trading:

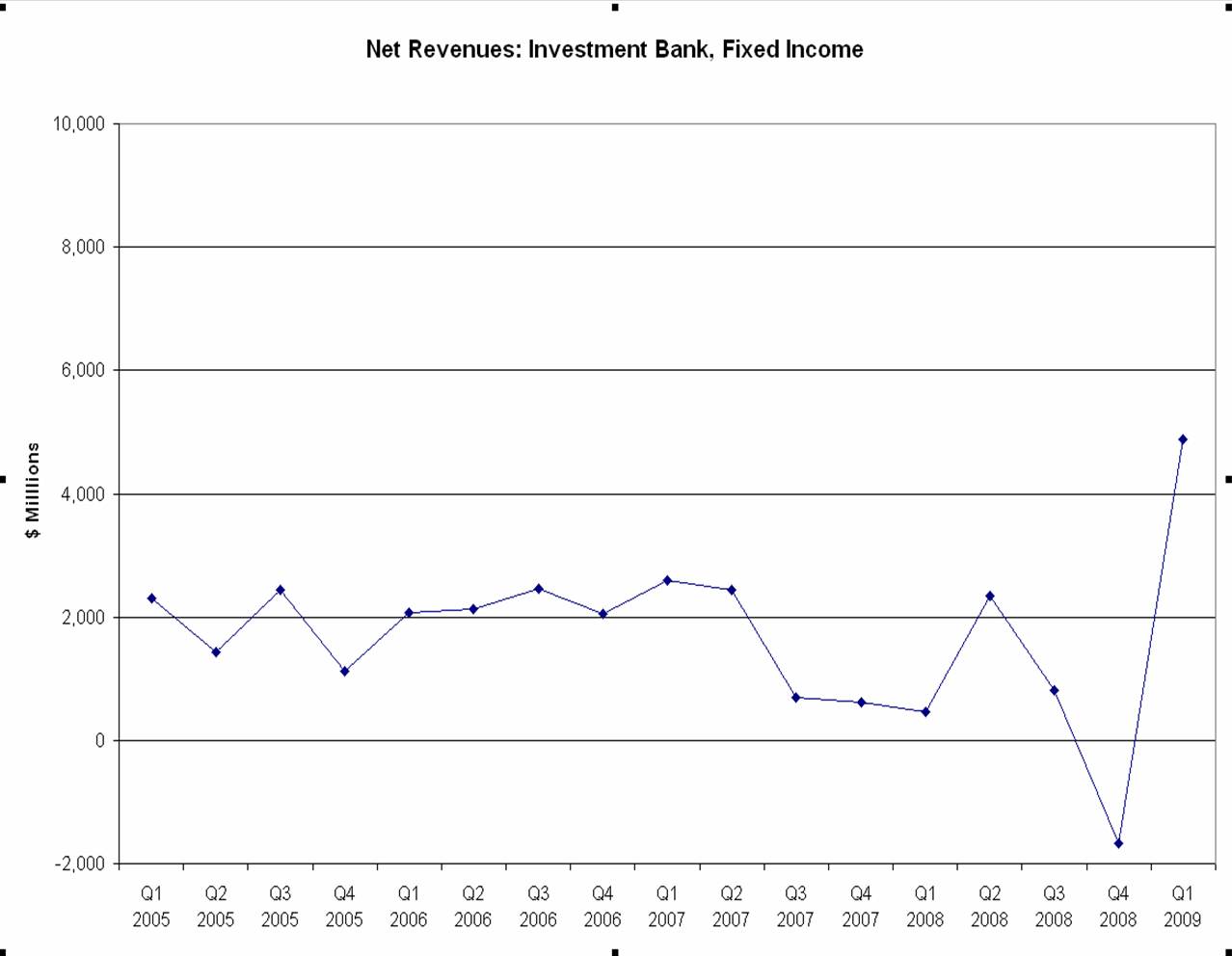

And here’s fixed income trading:

So for JPMorgan to reproduce these results quarter after quarter, it would have to have unprecedented, exceptional, super-duper fixed income trading revenues quarter after quarter. Now, JPMorgan’s prospects may be better than they were before the bust, since two major investment banks are gone, one of them absorbed into JPMorgan itself, meaning less competition and higher fees all around. But we also know that last quarter was a bit unusual because of the massive unwind at AIG, which hopefully will not be repeated.

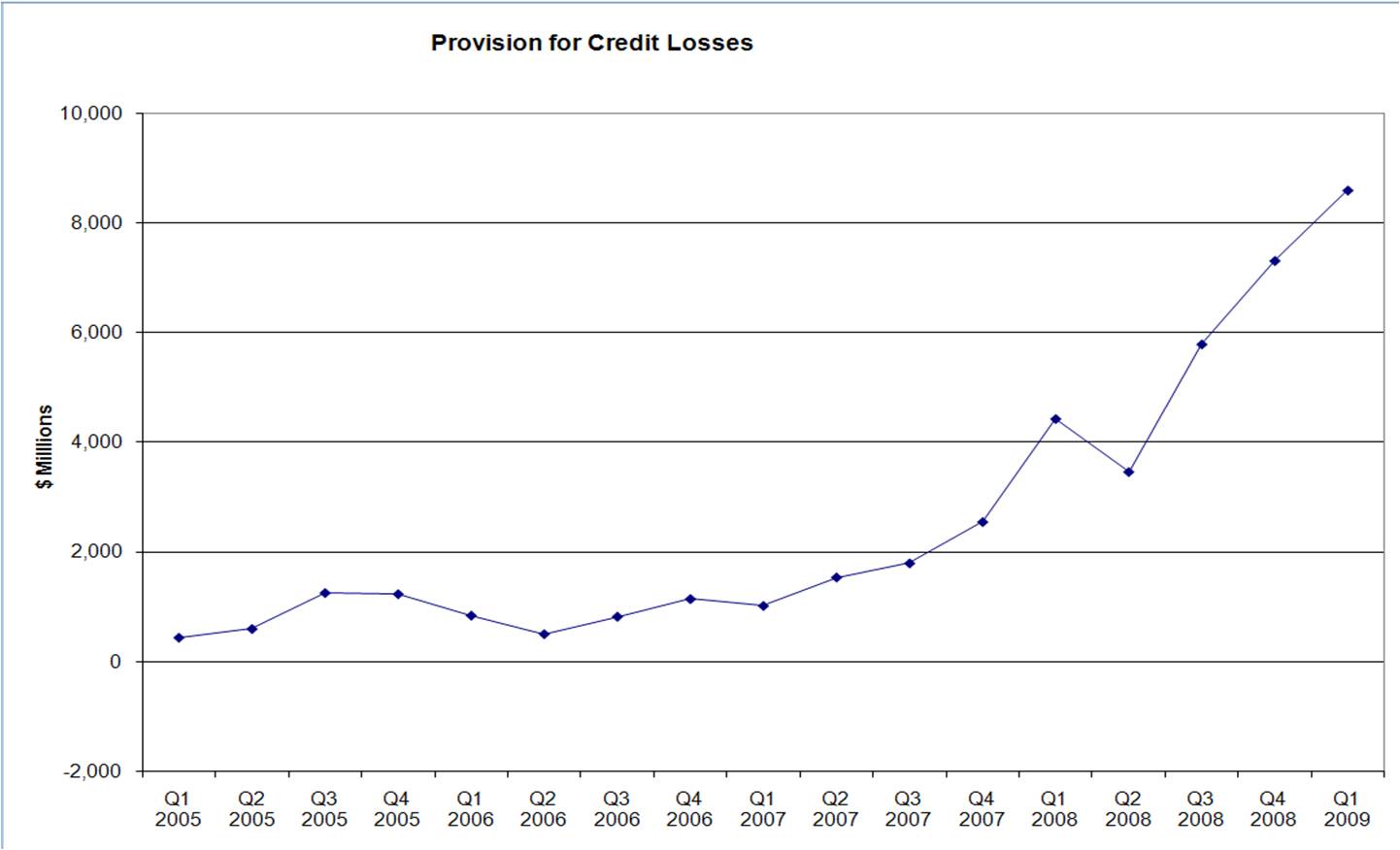

And here’s the dark side of the story: quarterly provisions for credit losses.

Note that these are income statement figures, so they are not cumulative: these are the provisions set aside each quarter, which should reflect the quarterly change in expectations about credit losses (defaults). The question is whether these big investment banks can make enough money from trading and fees to make up for the money they are still losing on credit exposures.

Note: I got my data from the financial supplements on this page. There’s a small discrepancy in the Q1 2006 numbers, depending on whether you look at the Q1 2006 release or the Q1 2007 release. But it’s only about $100 million, so I didn’t bother looking into it. |

|

狗仔卡

狗仔卡 发表于 2009-4-16 10:13 PM

发表于 2009-4-16 10:13 PM

提升卡

提升卡 置顶卡

置顶卡 沉默卡

沉默卡 喧嚣卡

喧嚣卡 变色卡

变色卡 发表于 2009-4-16 10:56 PM

发表于 2009-4-16 10:56 PM