|

|

本帖最后由 lilitulip 于 2020-8-23 04:37 PM 编辑

看了这篇文章这一段,实在很困惑,求解惑。 谢谢

尤其这里

What tends to be more predictive is the equity risk premium. (Equity risk premium is the additional return above a "risk-free" rate investors expect for putting their money into a riskier asset class.) You can proxy that as the earnings yield (the inverse of P/E) minus the 10-year Treasury yield.

https://www.fidelity.com/learnin ... ion-stocks-recovery

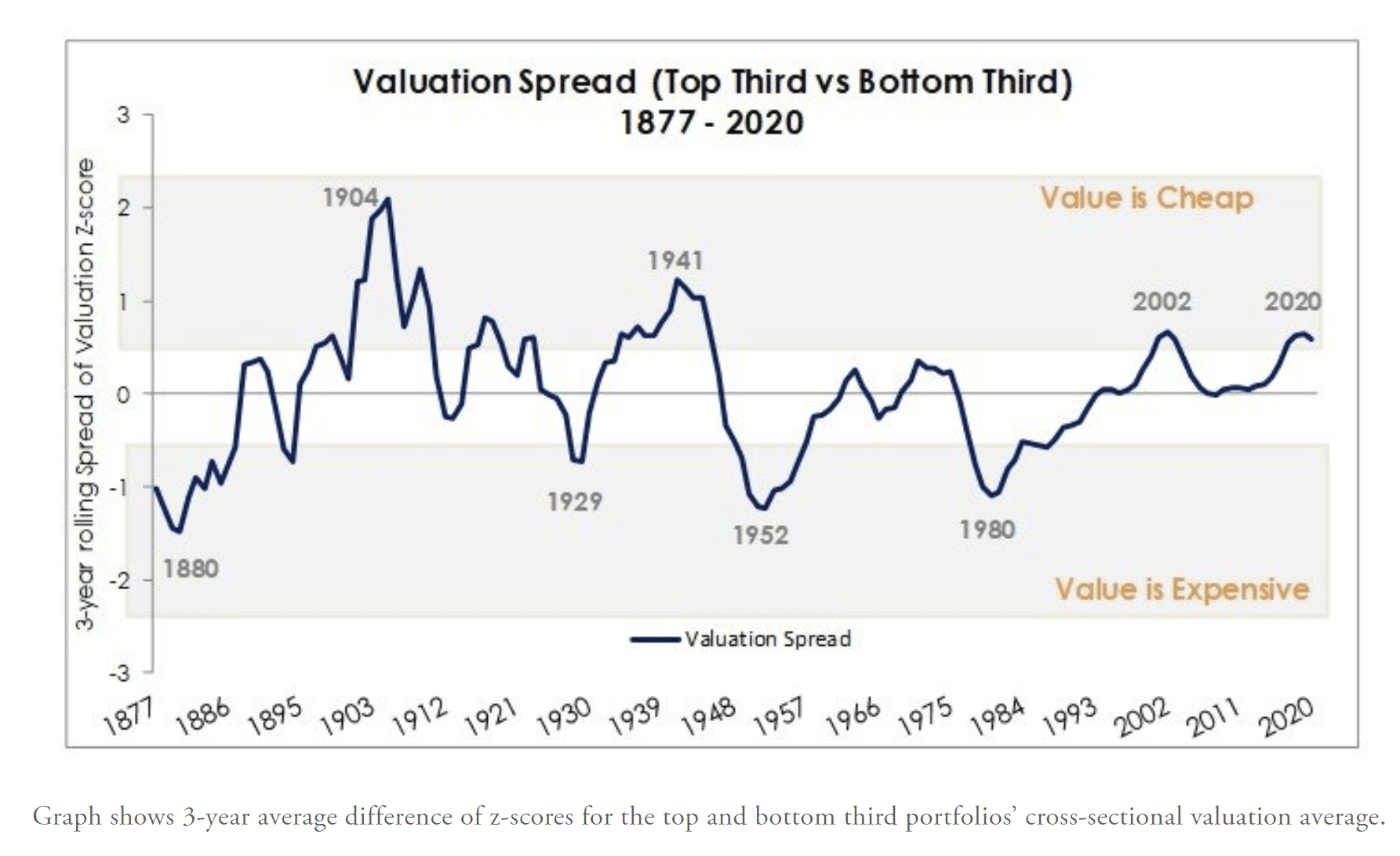

Do you think the market is overpriced given earnings?

Chisholm: I think that the tricky part about calling the market overpriced is defining it by price-to-earnings (PE). If you define it that way, the market's expensive. But it's important to realize how it got that way: on an unprecedented decline in earnings.

There are 2 problems associated with using P/E. First, stocks often get more expensive at earnings troughs, but earnings troughs are often coincident with a market bottom. 2009 offers an example. On P/E, stocks got pretty cheap, at 10x, before the true earnings decline hit. But multiples quickly rebounded to 15x as the earnings decline appeared. But it was the 15x valuation level, not the 10x, that coincided with the market rally. It coincided because that was the point at which earnings rebounded.

Second, earnings multiples overall are not very predictive of future returns on a 1- or 2-year basis. If we examine quartile data on valuation, stocks have the same odds of advancing regardless of which quartile they are in.

What tends to be more predictive is the equity risk premium. (Equity risk premium is the additional return above a "risk-free" rate investors expect for putting their money into a riskier asset class.) You can proxy that as the earnings yield (the inverse of P/E) minus the 10-year Treasury yield.

On that measure you start to see differentiated probabilities—the more expensive equities are relative to bonds, the lower the odds of an equity market advance. The situation we remain in, with stocks in their cheapest quartile relative to bonds, carries the highest odds of continued performance, at 84%.

When valuation measures conflict, I tend to lean on the ones that have been more predictive historically. And those continue to point toward a market advance. |

|

狗仔卡

狗仔卡 发表于 2020-8-23 05:35 PM

发表于 2020-8-23 05:35 PM

提升卡

提升卡 置顶卡

置顶卡 沉默卡

沉默卡 喧嚣卡

喧嚣卡 变色卡

变色卡 发表于 2020-8-23 05:52 PM

发表于 2020-8-23 05:52 PM